Microeconomics (Part 3E): (Step 3) Select Q (and associated P) to maximize Profit (Profit = Total Revenue – Total Cost)

Microeconomics

(Part 3E): (Step 3) Select Q (and associated P) to maximize Profit (Profit = Total Revenue – Total Cost)

a. Definition of Profit

- Profit = Total Revenue – Total Cost

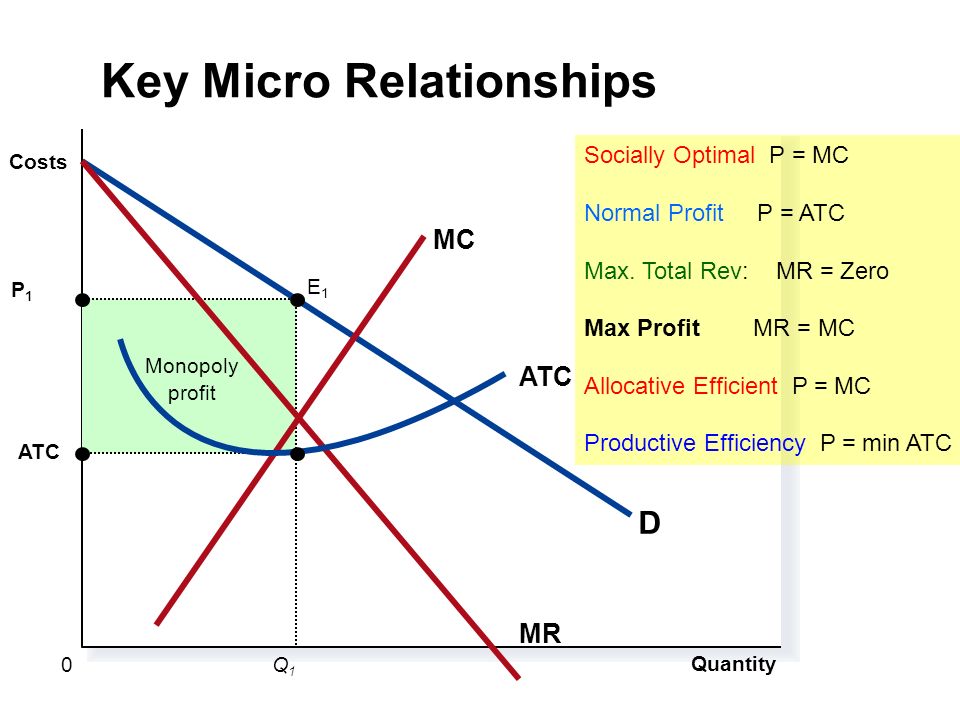

- Profit = (Price – Average Total Cost) Quantity

b. Profit Rectangle

- If the firm produces a quantity at which P > ATC, the

firm is profitable.

- If the firm produces a quantity at which P = ATC, the firm

breaks even.

- If the firm produces a quantity at which P < ATC, the

firm incurs a loss.

c. General optimum output rule: Q at MR = MC (Photo by ExpertsMind)

- According to the optimal output rule, profit is

maximized by producing the quantity of output at which the marginal revenue of

the last unit produced is equal to the marginal cost.

d. Price-taker (perfectly competitive firm)

- Total Revenue = Price x Quantity

- Profit = Total Revenue – Total Cost

- The profit-maximizing principle of marginal analysis:

the optimal amount of an activity is the level at which marginal benefit is

equal to marginal cost.

- The marginal revenue curve shows how marginal

revenue varies as output varies.

- According to the price-taking firm’s optimal output

rule, a price-taking firm’s profit is maximized by producing the quantity

of output at which the market price is equal to the marginal cost of the last

unit produced.

- Economic profit: the measure of profit based on the

opportunity cost of resources used in the business.

- Accounting profit: the profit calculated using only

the explicit costs incurred by the firm.

- If the firm produces a quantity at which P > ATC, the firm

is profitable.

- If the firm produces a quantity at which P = ATC, the firm

breaks even.

- If the firm produces a quantity at which P < ATC, the

firm incurs a loss.

Break-Even Price

- The break-even price of a price-taking firm is the

market price at which it earns zero profit.

- Whenever the market price exceeds minimum average

total cost, the producer is profitable.

- Whenever the market price equals minimum average

total cost, the producer breaks even.

- Whenever the market price is less than minimum

average total cost, the producer is unprofitable.

Summary

- Optimal Output Rule: Produce the quantity at which MR

= MC.

- For a price-taking firm, MR = P and its marginal

revenue curve is a horizontal line at the market price.

- Price-taking firm’s optimal output rule: produce

the quantity at which P = MC. However, a firm that produce the optimal quantity

may not be profitable.

- A firm is profitable if TR exceeds TC, or if market price exceeds

its break-even price (minimum ATC).

- If market price exceeds the break-even price, the

firm is profitable.

- If market price is less than the break-even price,

the firm is unprofitable.

- If the market price equals the break-even price,

the firm breaks even.

- When profitable, the firm’s per unit profit is P – ATC.

- When unprofitable, the firm’s per unit profit is ATC – P.

e. Price-maker

- A monopolist is the sole supplier of its good. Therefore,

the demand curve is simply the market demand curve (which slopes downward).

- The monopolist’s marginal revenue curve is always below

the demand curve.

- MR = MC at the monopolist’s profit-maximizing quantity

of output.

- P = MC at the perfectly competitive firm’s profit-maximizing

quantity of output.

- P > MR = MC at the monopolist’s profit

maximizing quantity of output.

In a competitive industry, a monopolist does the

following:

- Produces a small quantity: Q (monopoly) < Q (industry)

- Charges a higher price: P (monopoly) > P (industry)

- Earns a profit.

- At the monopolist’s profit-maximizing output level, marginal

cost = marginal revenue, which is less than market price.