Microeconomics

3C. (Step 1) Maximize Total Revenue (TR) for any given output (Q)

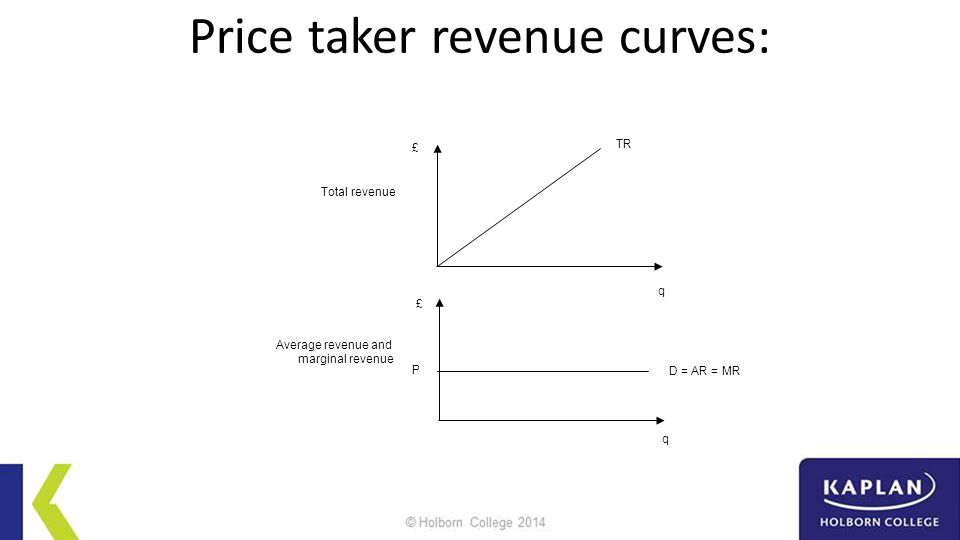

a. Total Revenue (TR) and Marginal Revenue (MR)

- Total Revenue = (The price of a good or service)

(Quantity sold)

- Marginal Revenue = The change in total revenue

generated by an additional unit of output

b. Relationship to elasticity and Marginal Revenue (MR)

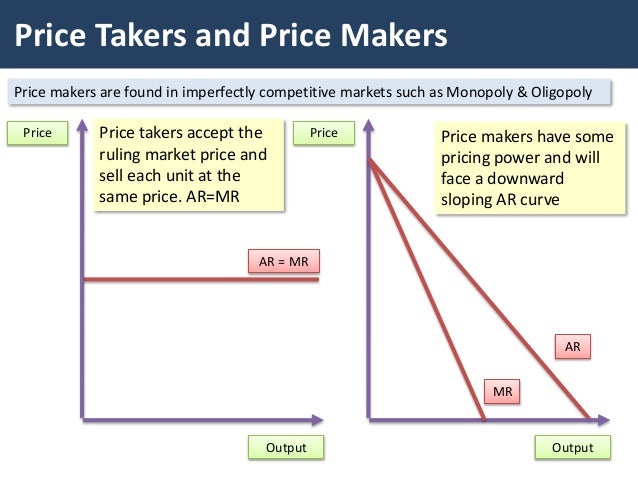

- The individual firm faces a horizontal, perfectly

elastic demand curve for its output – an individual demand curve for its

output that is equivalent to its marginal revenue curve.

c. Firm’s demand curve = Demand curve for firm’s product

d. For price-taker (perfectly competitive firm)

- A price-taking producer is a producer whose actions

have no effect on the market price of the good or service it sells.

- A price-taking consumer is a consumer whose

actions have no effect on the market price of the good or service he or she

buys.

- For an industry to be perfectly competitive, it must

contain many producers, none of whom have a large market share.

- For an industry to be perfectly competitive, consumers

regard the products of all producers as equivalent (standardized

product or commodity).

- Demand (D) curve = Marginal Revenue (MR) curve, market

price (P) = firm’s Marginal Revenue (MR)

Derivation of Total Revenue Curve (Photo by tutor2u)

e. For Price-Maker

- Price maker is any firm with market power

(downward-sloping demand curve)

- Market power is the ability of a producer to raise

prices.

- In a monopoly, a single uses its market power

to charger higher and produce less output than a competitive industry,

generating profits in the short and long run.

- Special case of monopoly: monopoly demand curve = market

demand curve

- Derivation of Total Revenue (TR) curve

Price-Taker Revenue Curves (Photo by Kaplan)

Additional Notes

- Neither the actions of a price-taking producer nor

those of a price-taking consumer can influence the market price of a

good.

- In a perfectly competitive market all producers and

consumers are price-takers. Consumers are almost always price-takers, but this

is often not true of producers. An industry in which producers are price-takers

is a perfectly competitive industry.

- A perfectly competitive industry contains many producers,

each of which produces a standardize product (also known as commodity)

but none of which has a large market share.

- Most perfectly competitive industries are also characterized

by free entry and exit.

- The marginal revenue of a monopolist is composed of

a quantity effect (the price reduced from the additional unit) and a price

effect (the reduction in the price at which all units are sold). Because of the

price effect, a monopolist’s marginal revenue is ALWAYS less than the

market price, and the marginal revenue curve lies BELOW the demand

curve.