2C. Supply Curve

Entities (Part 1)

- Entities are suppliers, sellers, producers, or

firms.

Horizontal Interpretation (Part 2)

Quantity Supplied (Part 2A)

- The quantity supplied is the actual amount of a

good or service people are willing to some specific price.

- The supply schedule shows the quantity supplied

depends on the price. The supply curve illustrates this relationship.

- The supply schedule shows the quantity supplied at

each price and is represented graphically by a supply curve. Supply

curves usually slope upward.

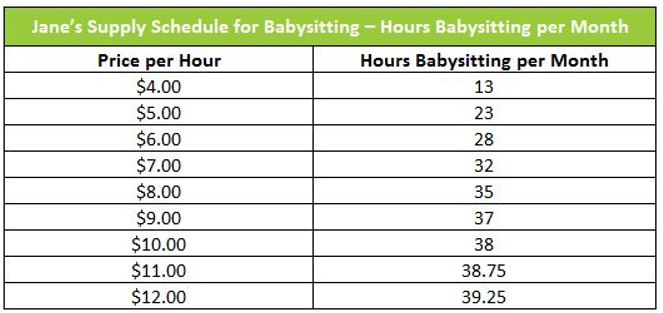

Supply Schedule vs. Supply Curve (Part 2B, Photo

by Higher Rock Education)

- A supply schedule shows how much of a good or

service would be supplied at different prices.

- A supply curve shows the relationship between

quantity supplied and price.

- An individual supply curve illustrates the

relationship between quantity supplied and price for an individual producer.

- The market supply curve is the horizontal sum of the individual

supply curves of all producers in the market.

- The supply schedule shows the quantity supplied

at each price and is represented graphically by a supply curve. Supply

curves usually slope upward.

- The market supply curve for a good or service is the horizontal sum of the individual supply curves of all producers in the

market.

Law of Supply (Part 2C)

- The law of supply states that an increase in price

results in an increase in quantity supplied.

Derivation of Market Supply Curve from Individual Supply

Curves (Part 2D, Photo by ResearchGate)

- To derive a market supply curve, we have to add the

supplies of all the producers of a product.

- Thus, the market supply of a good is the sum of

quantities of that good the individual firms are willing to offer for sale at a

given time period.

- The market supply is derived simply by adding the

quantities supplied at each price by the two producers.

- The market supply curve shows how the combined

total quantity supplied by all individual producers in the market depends on

the market price of that good.

Vertical Interpretation (Part 3)

Marginal Cost (Part 3A)

- Marginal cost is the additional cost incurred by

producing one more unit of a good or service.

- Marginal Costs = MC = seller’s cost = supplier’s cost.

- Marginal Cost = dollar value of what is given up producing

the marginal (last, next) unit.

- Marginal Cost = opportunity cost of producing that

additional unit.

- “Marginal Opportunity Cost” = minimum price at

which the supplier is willing to sell the unit.

Law of Increasing Marginal Cost (Part 3B)

- Law of Increasing Marginal Cost: Production of a

good or service has increasing marginal cost when each additional unit

costs more to produce than the previous one.

Formulas (Part 3C-3G)

- At any Quantity (Q), Marginal Cost (MC) curve shows

Marginal Cost of last unit.

- Producer (P) net gain from ith unit = Price –

Marginal Costi

- Producer surplus (or profit) = Sum (Price – Marginal Costi)

= Sum (Price – Quantityi)

- Decision Rule: Given Price, select Quantity to maximize

Producer Surplus -> Quantity at Price = Marginal Cost

- Marginal Cost curve is supply curve, given rational behavior

(maximize Producer Surplus), law of increasing cost, parametric behavior with

respect to price.

- Supply Curve is Marginal Cost curve: height of Supply

Curve is Marginal Cost of that unit.

- There are both individual and market marginal cost curves.

- The marginal cost has an effect on the Producer Surplus of

change in price.

Vocabulary

- The demand curve for a good is determined by each

potential consumer’s willingness to pay.

- Individual Consumer Surplus is the net gain an

individual consumer gets from buying a good.

- The total consumer surplus in a given market is

equal to the area below the market demand curve but above the price.

- A fall in the price of a good increases consumer

surplus through two channels: (1) a gain to consumers who would have bought

at the original price and (2) a gain to consumers who are persuaded to buy by

the lower price. A rise in the price of a good reduces consumer surplus in a

similar fashion.

- A seller’s cost is the lowest price at which he or

she is willing to sell a good.

- The supply curve for a good is determined by the cost

of each seller.

- The difference between the price and cost is the seller’s individual

consumer surplus.

- The total producer surplus is equal to the area

above the market supply curve but below the price.

- The cost of each potential producer, the lowest

price at which he or she is willing to supply a unit of a particular good,

determines the supply curve.

- The term producer surplus is often used to refer to

both individual and total producer surplus.

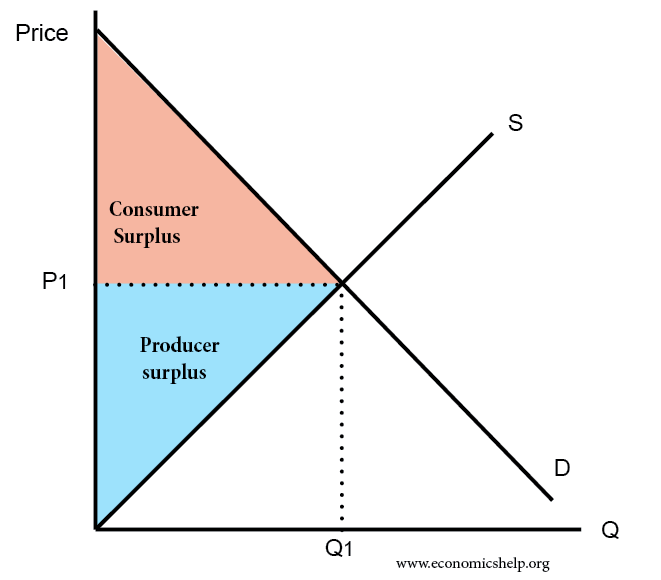

Producer Surplus (Photo by EconomicsHelp)

- Individual producer surplus is the net gain to an

individual seller from selling a good. It is equal to the difference between

the price received and the seller’s cost.

- Total producer surplus is the sum of the individual

producer surpluses of all of the sellers of a good in a market.

- Economists use the term producer surplus to refer

both individual and to total producer surplus.

- The total producer surplus from sales of a good at a given

price is the area above the supply curve but below the price.

Shifts of Supply Curve (Part 4, Photo by CourseHero)

Shift of the Supply Curve (Part 4A)

- A shift of the supply curve is a change in the

quantity supplied of a good or service at any given price. It is represented by

the change of the original supply curve to a new position, denoted by a new

supply curve.

- A movement along the supply curve is a change in

the quantity supplied of a good arising from a change in the good’s price.

Outward, Right, Downward vs. Inward, Leftward, Upward

(Part 4B)

- A rightward shift of the supply curve means at any

given price; producers supply a larger quantity of the good than before.

- A leftward shift of the supply curve means

at any given price; producers supply a smaller quantity of the good than

before.

- An input is a good or service that is used to

produce another good or service.

- Increases or decrease in supply lead to shifts of the

supply curve. An increase in supply is a rightward shift: the quantity

supplied rises for any given price. A decrease in supply is a leftward shift:

the quantity supplied falls for any given price.

Shift Due to Change in Marginal Cost versus Other Reason

(Part 4C)

- Shifts of the supply curve dis a change in the

quantity supplied at any given price.

Causes in Shift (Part 4D)

- The five main factors that shift the supply curve are:

(1) A change in input prices

(2) A change in the prices of related goods and services

(3) A change in technology

(4) A change in expectations

(5) A change in the number of producers